Private Equity Market Update

Updates at a Glance — May 2022

Market Trends

- Market Overview Q1 2022 — Inflation, Interest Rates and Geopolitical Uncertainty

- U.S. Private Equity Deal Activity Q1 2022

Key Transaction Considerations

M&A:

- M&A Deal Terms — Potential Geopolitical Impacts

- R&W Insurance — Geopolitical Exclusions

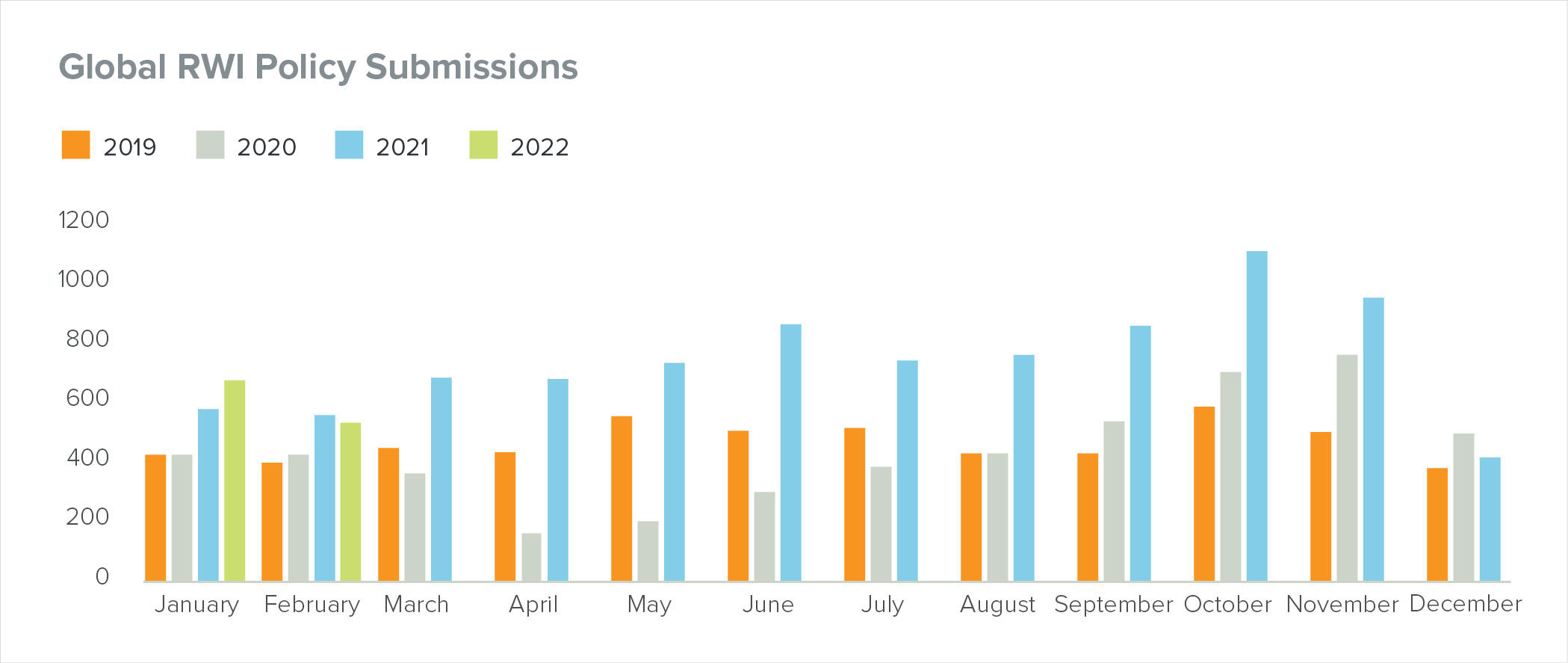

- Goodwin Private Equity Database — U.S. Buyers, Don’t Miss Your Deadline for the Closing Statement

- Portfolio Company Management Incentive Plans — Implications of Russian Sanctions & Sanctions Timeline

ESG:

Market Overview — Q1 2022

Private equity deal making in 2021 surpassed historical records across a number of metrics despite COVID-19 headwinds, supply chain volatility and labor shortages.

M&A Challenges: While many of those challenges remain in place, the start of 2022 introduced new uncertainties to deal making — the Russian invasion of Ukraine, appropriately heightened focus on cybersecurity, historically high inflation levels and the Federal Reserve Board’s approval of a 25bp interest rate increase in March (with additional raises anticipated this year), to name a few.[1]

Inflation: Year-over-year Consumer Price Index remained above 5% during the second half of 2021 and has climbed beyond 8% in 2022[2] at the fastest 12-month pace since 1981[3], fueled by, among other things, rising gas prices exacerbated by the war in Ukraine and rising vehicle costs as a result of COVID-19-induced flight from cities and the global semiconductor shortage. The effect of inflation on middle market deal-making activity will vary by industry and by the ability of companies within negatively impacted industries to pass on increased input costs to customers, solve supply chain issues and achieve other operational gains.

Volatility in the Debt Market: 2021 private equity dealmaking benefited from the availability of cheap LBO financing, however, with further interest rates rises anticipated this trend may be curtailed. Q1 2022 headwinds saw high-yield bond offerings and syndicated leveraged loan issuances pull back, although as of the date of this update such markets have started to open back up.

Private Credit: Sponsors are likely to still have plenty of access to capital due in large part to the growth of the private credit market, which has remained fairly active. Private credit lenders continue to chip away at the large-cap market historically dominated by investment banks, as evidenced by a number of recent private credit unitranche facilities in excess of $1 billion, a continuing and growing trend, particularly in the technology and software sectors.

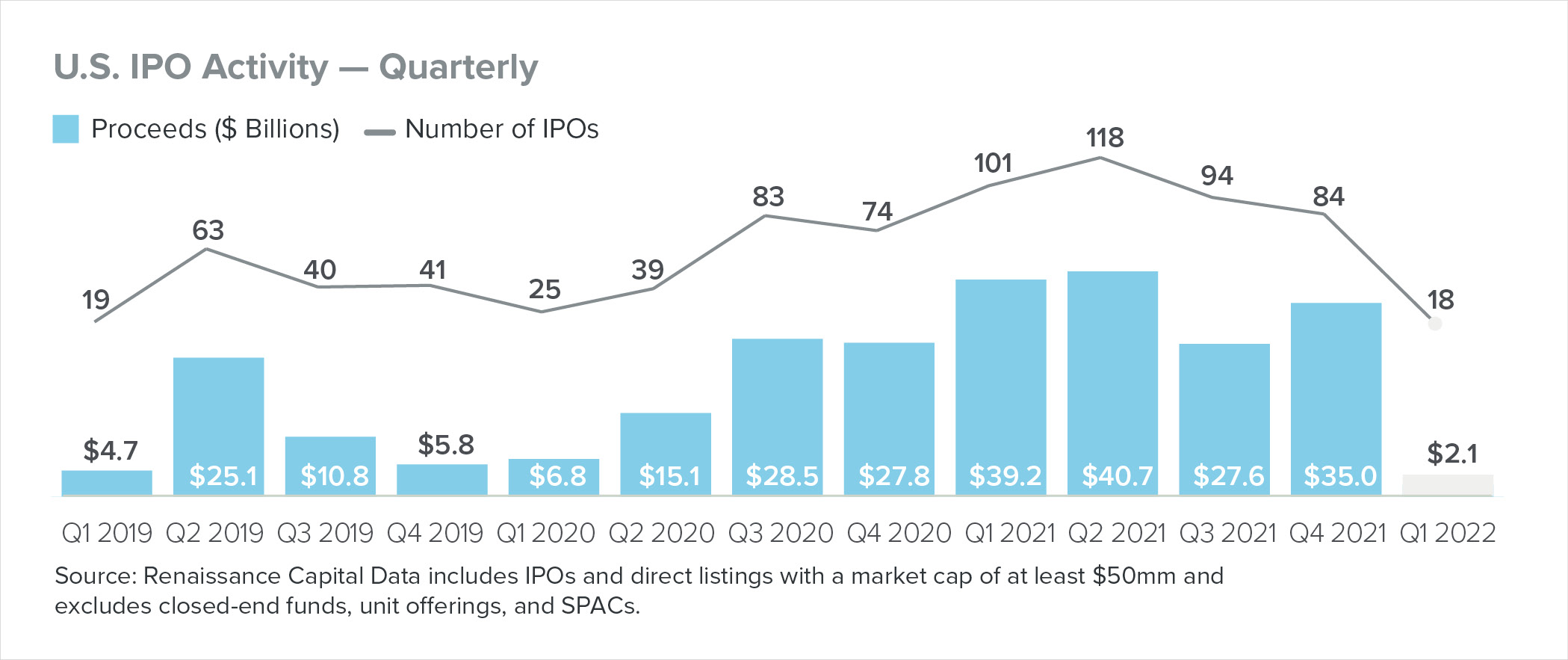

Public Markets and Valuations: The U.S. IPO market had its slowest first quarter in six years, with only 18 IPOs raising $2.1 billion[4]. Rising interest rates and the pressure on valuations were reflected in the public and private markets where a number of high growth companies saw their trading price cut by as much as half[5]. High growth tech stocks were particularly impacted, creating opportunity for middle market private equity firms seeking to secure more reasonable valuations.

To view a larger version, please click here.

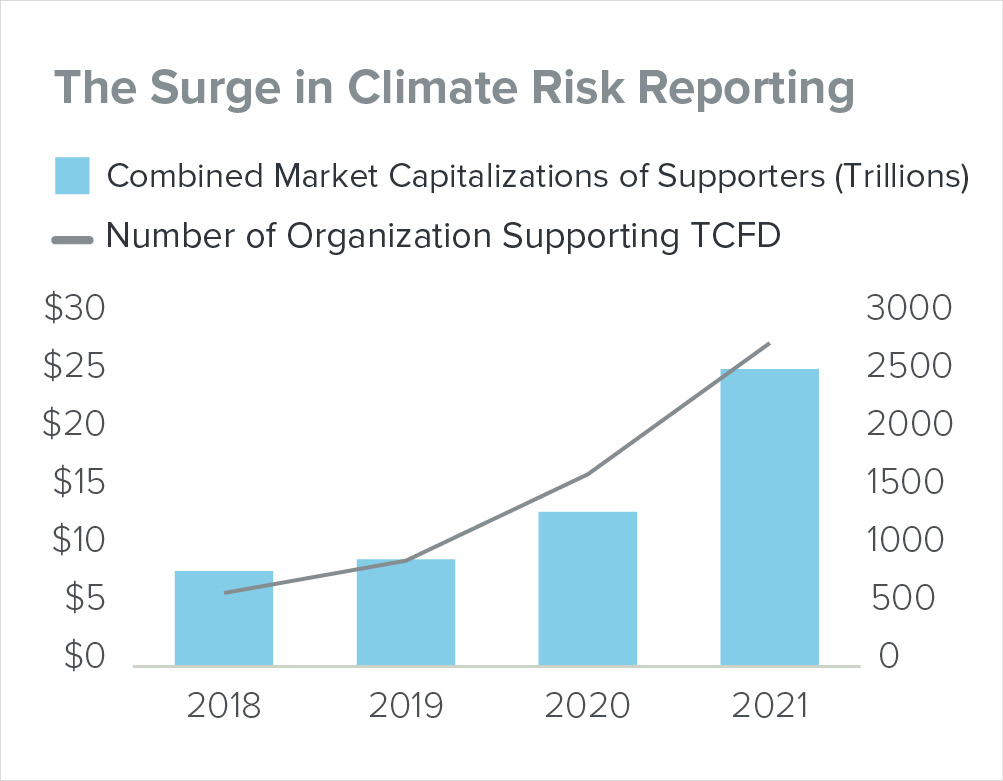

U.S. Private Equity Transactional Activity

U.S. Private Equity M&A

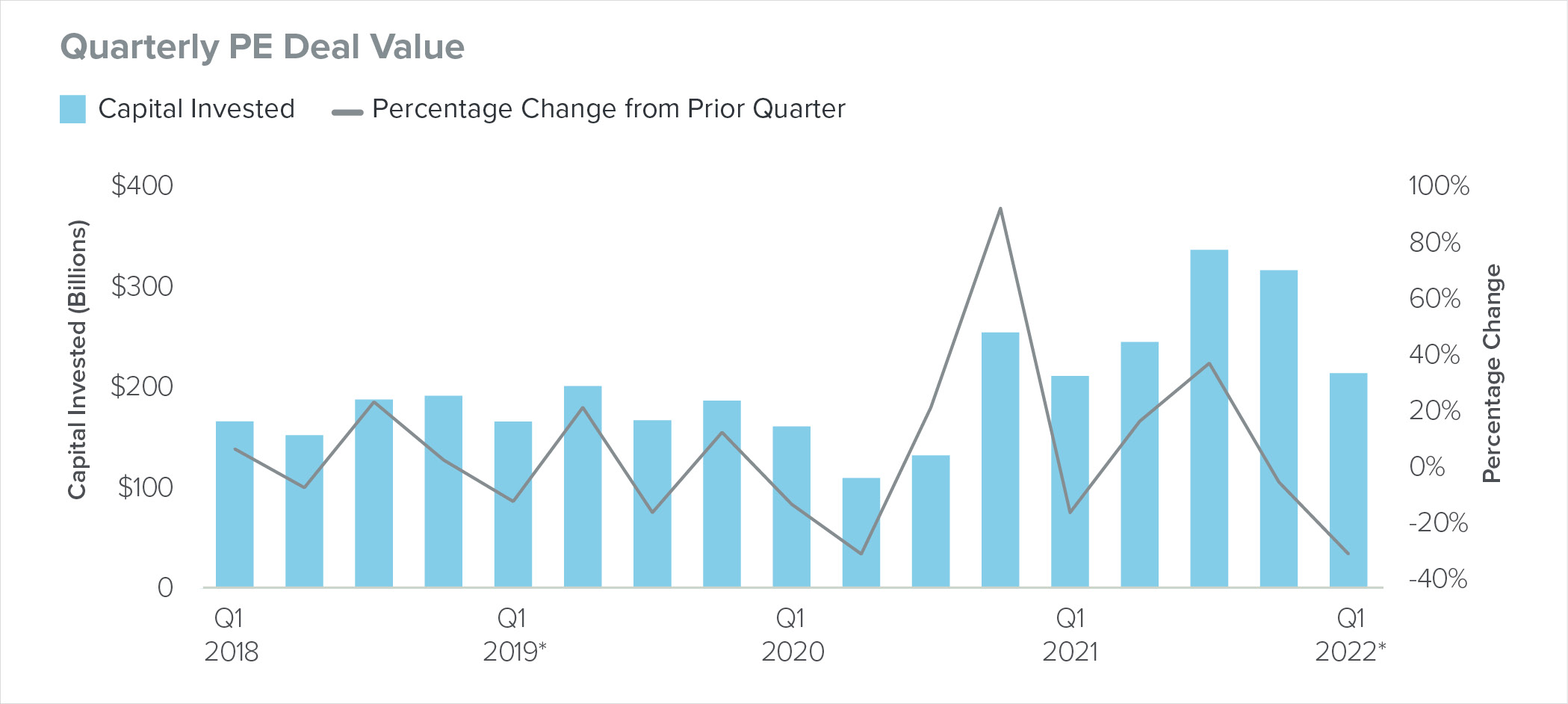

Deal Activity: Total capital invested across U.S. private equity buyout and growth equity transactions[6] remained higher in Q1 2022 in absolute terms than Q1 2021, but declined by 32% compared to Q4 2021[7].

Source: Pitchbook. Goodwin analysis.

To view a larger version, please click here.

{kind=link}

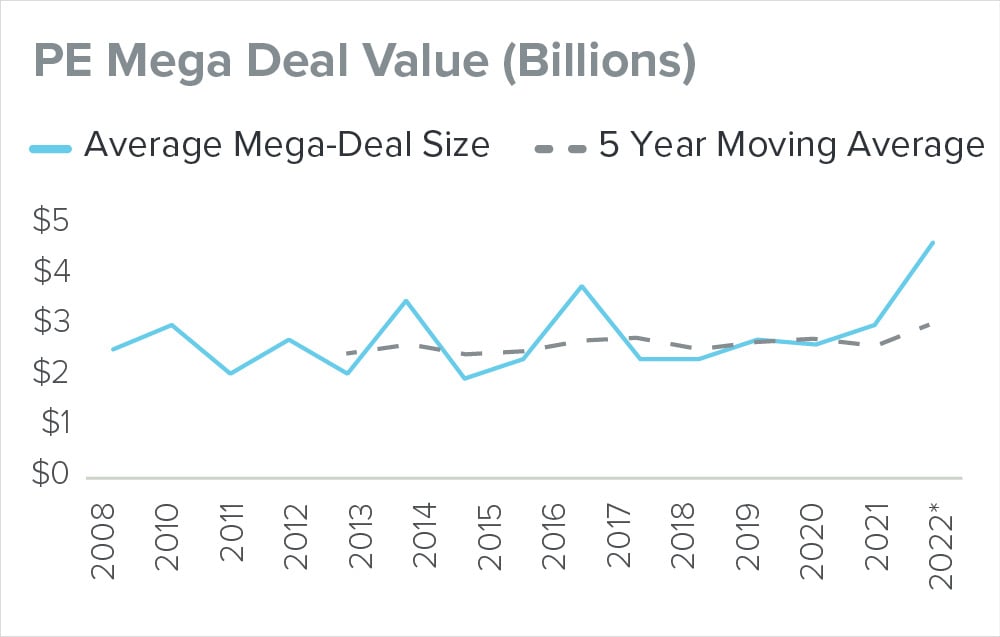

Mega-Deals: Mega-deal[8] activity continued to take on an even greater share of private equity deal making in Q1 2022, representing 36% of capital invested.

Although average deal sizes for mega-deals have stayed fairly consistent over the last four years, Q1 2022 saw a surge in average deal size relative to both the prior quarter and the long-term multi-year average[9], driven by a smaller number of higher value transactions.

Source: Pitchbook. Goodwin analysis.

To view a larger version, please click here.

U.S. Private Equity Exit Activity

Exit Activity: Public listings, which drove private equity exit activity in 2021, came to a halt. Overall, private equity exit value and deal count decreased compared to Q4 2021 by 57.5% and 57.2%, respectively. Exit activity was also lower than Q1 2021 by 40.3% in terms value and 16.4% by deal count[10]. As a result of public market volatility and shifting market appetite for de-SPAC transactions, sponsor-to-sponsor exits instead represented the majority of Q1 exit activity as many private equity firms looked to deploy dry powder. Similar to deal activity, mega exits[11] represented a larger share of total private equity exit activity in Q1.

M&A Transaction Considerations

Geopolitical Impact on Deal Terms and R&W Insurance

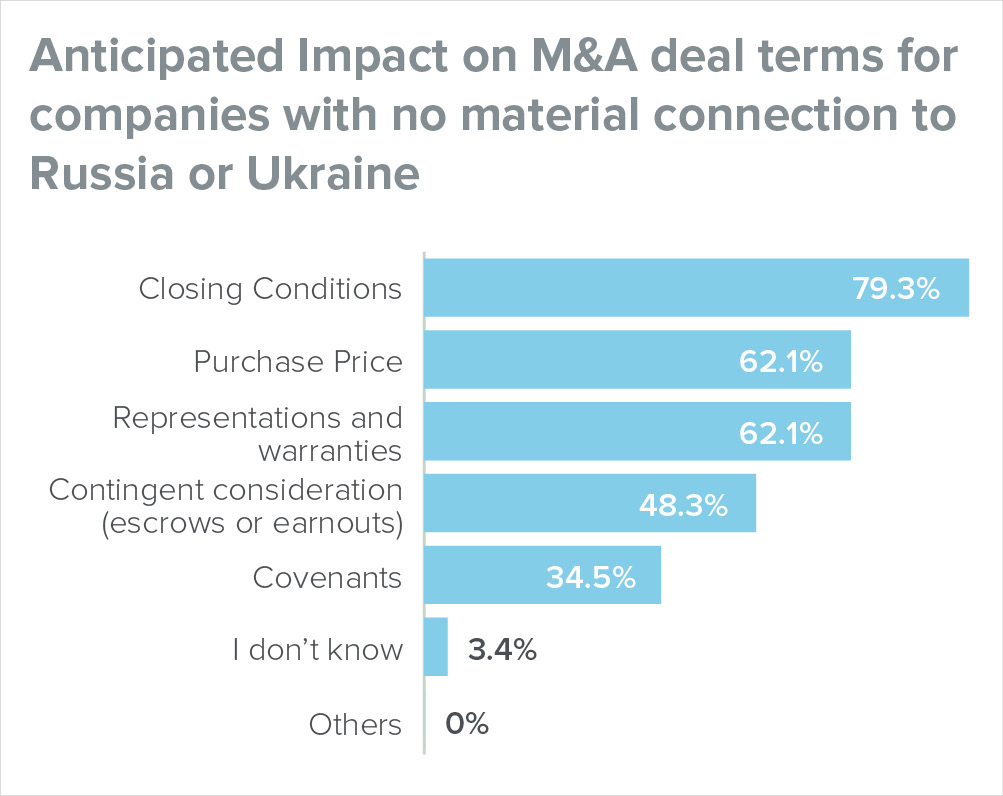

Deal Terms: In a survey conducted by SRS, only 30% of respondents believe that the invasion of Ukraine will affect M&A deal terms for companies that do not have a material connection to Russia or Ukraine. Of those who believe that deal terms will be impacted: 79% believe this impact will be to closing conditions; 62% to the purchase price and 62% to the representation and warranties[12].

Source: Interest Rates, Ukraine, and M&A Impacts, SRS Report To view a larger version, please click here.

R&W Insurance

Pricing and Capacity: Compared to the second half of 2021 when the rate on line (premium divided by the policy limit) kept climbing up (sometimes exceeding 5%), average R&W policy rates in North America now fall around 4-5% for most deals. Cyclical downturn in Q1 2022 vs. Q4 2021, as reflected in the number of policies bound by underwriters, is indicative of increased underwriting capacity and widening of options. The volume of deals seeking R&W insurance in early 2022 is comparable to early 2021 levels.

Source: Euclid Transactional

To view a larger version, please click here.

Exclusions: The Russian invasion of Ukraine has caused insurers to scrutinize any Russian ties in transactions and to ask more specific questions as part of their standard underwriting process. Some insurers have broad mandatory exclusions related to Russia, Ukraine and Belarus, in addition to economic sanctions exclusions already included in policies, while others take a case-by-case approach based on identified links to operations and counterparties in those jurisdictions. This is akin to COVID-19-related questions asked in every deal and COVID-19-related policy exclusions, which remain in policies in varying degrees.

U.S. Buyers, Don’t Miss Your Deadline for the Closing Statement

A recent Delaware Court of Chancery summary judgement motion[13] held that a buyer who missed the customary deadline set forth in the purchase agreement to deliver the post-closing statement within 90 days of closing waived its right to do so. As a result, the buyer lost its right to a downward purchase price adjustment and the seller was entitled to keep the funds held in the purchase price adjustment escrow. Holding otherwise, the court notes, would reward the buyer for breaching the purchase agreement.

Source: Goodwin Private Equity Deal Database

To view a larger version, please click here.

According to the 2021 ABA Private Deal Point study[14] (i) 80% of deals were silent on the implications of missing the deadline for a post-closing statement and (ii) 14% of deals provided that the estimated closing statement delivered at closing would become final if the deadline for the post-closing statement was missed.

Buyers should ensure that they have sufficient time post-closing to prepare the post-closing statement, and that supporting advisors are aware of the deadline in order to minimize the risk of failure to deliver on time. Our Private Equity Deal Database shows that the preparer of the post-closing statement (typically the buyer) generally has 90 days to prepare the statement after closing. Specifics should be included in the purchase agreement to address what happens in the event that the buyer misses the deadline and how missing that deadline may be remedied (e.g., a missed deadline that does not prejudice the seller does not waive the right of the buyer to deliver the post-closing statement).

Portfolio Company Management Incentive Plans — Implications of Russian Sanctions

In light of Russia’s invasion of Ukraine, domestic and international sanctions regimes against Russia continue to evolve. Our sanctions timeline provides a high-level overview of the key sanctions implemented by the U.S. and the types of sanctions imposed. Penalties for violating U.S. sanctions can be severe. Clients should familiarize themselves with potentially applicable sanctions and should conduct thorough due diligence on targets to determine whether a particular type of business activity may be subject to sanctions.

In response to the sanctions against it, Russia has passed its own countermeasures. In particular, share issuances and the granting of equity incentives by U.S. companies to Russian nationals (regardless of tax residency or location) are now caught under the new countermeasures.

As the situation is highly complex and likely to continue to evolve, sponsor clients should contact us if the circumstances below arise:

- New equity grants to employees located in Russia/Belarus or to Russian nationals (regardless of location and tax residency) are contemplated; and

- Existing equity plans are in place between portfolio companies and employees that are located in Russia/Belarus or Russian nationals (regardless of location and tax residency).

Tracker of U.S. Sanctions and Export Controls on Russia

Financial

Financial  Individual

Individual Travel

Travel

| April 21 | Russian-affiliated vessels prohibited from entering U.S. ports. |  |

| April 20 | Visa restrictions placed on hundreds of individuals. Sanctions placed on individuals and entities attempting to evade U.S. sanctions. |

|

| April 8 | MFN status (normal trade relations) with Russia and Belarus suspended. Prohibition on imports of energy products from Russia. Additional license requirements placed on exports to Russia & Belarus. |

|

| April 7 | Sanctions placed on Russia’s largest diamond mining company and a major company building Russian warships. Enforcement actions taken against three Russian airlines operating in violation of U.S. export controls. |

|

| April 6 |

Full blocking sanctions imposed on Sberbank. Sanctions imposed on family members of Putin and Lavrov. New investment and provision of certain services in the Russian Federation banned. |

|

| April 1 | Export controls expanded by adding 120 Russian and Belarus entities supporting the Russian military. | |

| March 31 | Additional sanctions imposed on individuals involved in Russian sanction evasion networks & three major Russian technology companies. | |

| March 24 | Sanctions imposed on 48 Russian defense companies, the State of Duma, 328 members of the State of Duma, and the CEO of Public Joint Stock Company Sberbank of Russia. |

|

| March 16 | REPO multilateral task force launched to enforce sanctions on Russian elites & oligarchs. Prohibition on exports of luxury goods to Russia and imports from Russia in several sectors. |

|

| March 11 | White House to work with G7 leaders to prohibit Russia from borrowing from IMF, the World Bank and other financial institutions. Sanctions imposed on additional Russian elites. |

|

| March 8 | Prohibition on imports of Russian oil, liquified natural gas and coal. | |

| March 3 | Sanctions imposed on 22 Russian defense-related entities, additional Russian elites & other individuals and entities involved with spreading misinformation. Additional export controls imposed on Russian oil refinery sector. |

|

| March 2 | Belarus subject to the same export control restrictions as Russia. Task Force KleptoCapture established to enforce U.S. sanctions, export restrictions and other economic countermeasures. Russian air travel in U.S. airspace suspended. |

|

| February 28 | Prohibition on transacting with the Central Bank of Russia, the National Wealth Fund of Russia, and Russia’s Ministry of Finance (with an exception for certain energy-related transactions). Sanctions imposed on Russian Direct Investment Fund and its CEO |

|

| February 26 | Russian Banks removed from SWIFT. Transatlantic taskforce established to identify and freeze assets of sanctioned parties. |

|

| February 25 | Sanctions imposed on Putin & Lavrov | |

| February 24 | Sanctions imposed on additional major Russian financial institutions, individuals & entities. Restrictions placed on exports to Russia of technologies that are essential inputs to Russian defense, aerospace and maritime sectors |

|

| February 22 | Sanctions imposed on two major Russian state-owned financial institutions and five Russian oligarchs. Additional restrictions imposed on the market for Russian sovereign debt. |

|

| February 21 | Trade & investment embargo on two Ukraine regions recognized by Russia. | |

Sources: Peterson Institute for International Economics, Russia’s war on Ukraine: A Sanctions Timeline, Chad P. Brown. Thompson Reuters Practical Law, U.S. Sanctions and Export Controls on Russia: Tracker

ESG Transaction Considerations

Proposed Climate Disclosures

On March 21 2022, the SEC proposed rule changes that, if passed, would require public companies to report the climate-related risks of their business activities (“Proposed Climate Disclosures”) across four core areas: (i) governance; (ii) business and financial statements; (iii) strategy and business model; and (iv) climate-related events (see below).

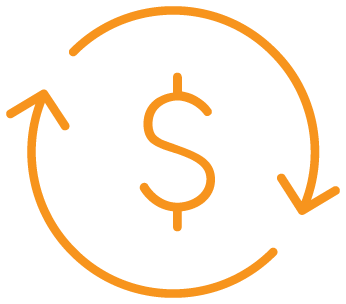

Demand for Climate Reporting: The Proposed Climate Disclosures are similar to those that many companies already provide based on broadly accepted disclosure frameworks, such as the Task Force on Climate-Related Financial Disclosures (“TCFD”) and the Greenhouse Gas Protocol. Support for the TCFD has grown five-fold in three years and is currently supported by 2,616 organizations with a combined market capitalization of $25 trillion[15].

The Proposed Climate Disclosures have been driven in part by the global shifts from voluntary to mandatory climate related regimes (e.g., Hong Kong, EU and UK); demand by consumers and institutional investors for consistent and transparent reporting metrics and to abate greenwashing concerns. The Proposed Climate Disclosures are still open to public commentary and may be challenged based on the SEC’s authority to implement such rules.

Potential Implications for GPs

- GPs considering exits via the public markets or to public companies may need to consider how Proposed Climate Disclosures will be managed if the proposed rules are passed (see approval and implementation timeline below).

- Given the growing convergence between private market initiatives (e.g. the Data Convergence Project which currently has 140 participating members)[16] and public market initiatives to track carbon/climate related risks, developing a carbon footprint strategy for portfolio companies and engaging management teams early may be advisable.

- Implementation of the rules will likely create a regulatory arbitrage between the private and public markets and result in greater public to private transactions.

- As a result of the proposed rule for certain public companies to report scope 3 emissions, portfolio companies in public company value chains will likely need to assist with the provision of data and over time their emissions may be more closely monitored.

Source: TCFD 2021 Status Report

To view a larger version, please click here.

{kind=link}

Overview of Proposed Climate Disclosures

The Proposed Climate Disclosures would require companies to disclose information in their registration statements (Forms S-1, S-3, F-1 and F-3) and periodic reports (Forms 10-K, 10-Q and 20-F) in relation to the following areas.

| Proposed Climate Disclosures | |

| Governance | Oversight and governance procedures of climate-related risks by a company’s board and management. |

| Business and Financial Statement Impacts | How any climate-related risks identified by the company have had or are likely to have a material impact on its business and consolidated financial statements, which may manifest over the short-, medium-, or long-term. |

| Strategy and Business Model | How any identified climate-related risks have affected or are likely to affect a company’s strategy, business model and outlook. |

| Financial Statements | The impact of climate-related events (severe weather events and other natural conditions) and transition activities on the line items of a company’s consolidated financial statements, as well as on the financial estimates and assumptions used in the financial statements. |

| GHG Emissions | Reporting of scope 1 (direct emissions), scope 2 (indirect emissions) and scope 3 emissions (emissions from upstream and downstream activities); in some cases an attestation report from an independent GHG provider will be required. |

| Approval Timeline | The 60-day period for public comment will end on May 20, 2022 before final approval can be granted. The proposed rule may be challenged in court. |

| Implementation Timing | If adopted, the proposals would likely take effect in the fiscal year 2023 and apply to SEC filings in 2024, with a phase period outlined in the Fact Sheet. |

[1] Source: Federal Open Market Committee

[2] Source: According to Pitchbook, U.S. PE Middle Market Report 2021 Annual

[3] Source: NYTimes, Inflation Hits Fastest Pace Since 1981, at 8.5% through March, Jeanna Smialek

[4] Source: Renaissance Capital

[5] Source: According to Pitchbook, U.S. PE Middle Market Report 2021 Annual

[6] This data includes non-control deals.

[7] Source: PitchBook; Goodwin analysis

[8] Transactions with enterprise value of $1billion+

[9] Source: Pitchbook. Goodwin analysis.

[10] Source: PitchBook U.S. PE Breakdown Q1 2022

[11] Exits with enterprise value of $1bn+

[12] Source: Interest Rates, Ukraine, and M&A Impacts, SRS Report

[13] Source: (Schillinger Genetics, Inc.) Download.aspx (delaware.gov)

[14] Source: Private Target Mergers & Acquisitions Deal Points Study, a project of the M&A Market Trends Subcommittee of the Mergers & Acquisitions Committee of the American

Bar Association Business Law Section.

[15] Source: TCFD 2021 Status Report.

[16] https://www.goodwinlaw.com/-/media/files/publications/pe-thought-leadership/1_pemarketupdateseriestlesgjan22127318v2.pdf